Why Global Companies Are Moving Manufacturing to India: 7 Structural Reasons

Introduction

Apple. Foxconn. Micron. Airbus. Rolls-Royce. Suzuki. These are not companies chasing a trend – they are global category leaders making 10-year supply chain commitments. What do they all see in India? Seven structural forces are converging to make India the dominant manufacturing destination of the next decade. This article unpacks each one – with data, not platitudes.

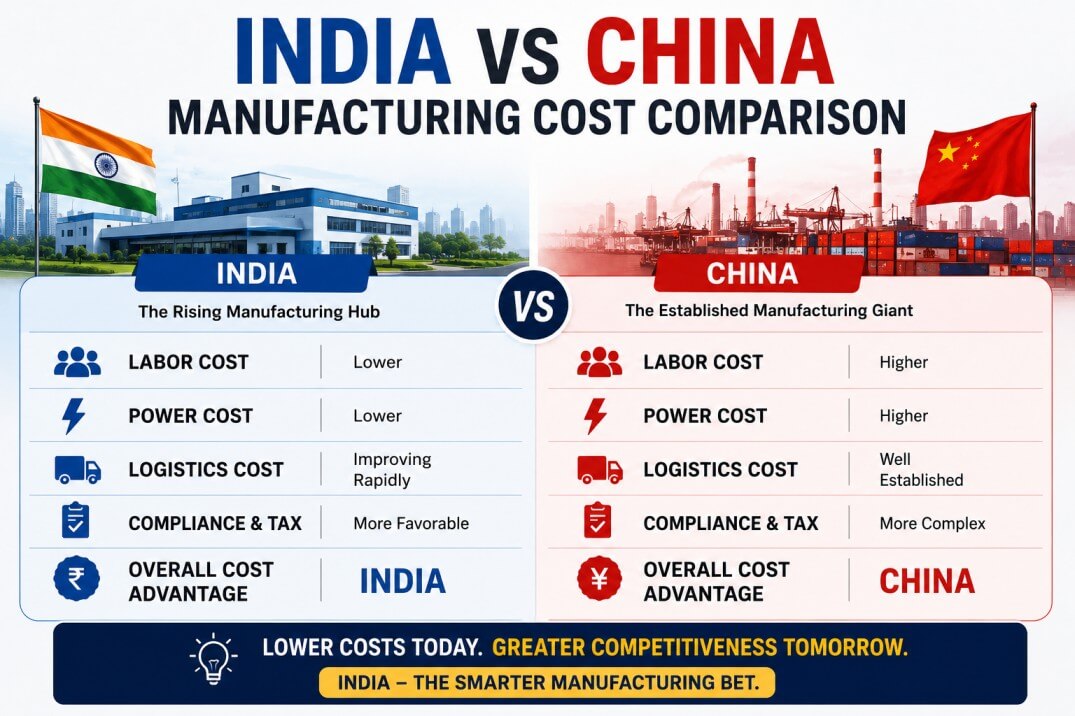

Reason 1: Demographics – The Only Large Young Workforce in the World

China’s working-age population peaked in 2015 and is declining. Vietnam, Thailand, and Malaysia are ageing. Bangladesh is running out of rural labour surplus.

India has 940 million people of working age (15-64) and adds approximately 12 million new workers per year. Median age: 28.4 years. By 2047, India’s workforce will be the largest in the world.

For labour-intensive manufacturing – electronics assembly, garment production, auto components, food processing – demographic advantage is structural and durable. The wage rate advantage over China is backed by a labour supply that will sustain it for 15-20 years.

Reason 2: Government Policy – The Most Pro-Manufacturing Policy Stack in India’s History

Three interlocking policy instruments:

- PLI schemes (Rs 2 lakh crore across 14 sectors): Pay companies to produce in India. Already deployed in mobile phones, semiconductors, pharma, textiles, specialty steel, automobiles, and food processing.

- ECMS 2025 (Rs 22,919 Cr): Build the electronics component supply chain that PLI-driven assembly revealed as a gap.

- India Semiconductor Mission (Rs 76,000 Cr): Attract semiconductor wafer fab and OSAT investment. Micron (OSAT), Tata (fab), CG Power (OSAT) have all committed.

This is the first time in India’s post-independence history that government policy has been this consistently, persistently pro-manufacturing investment – and backed by capital rather than just rhetoric.

Reason 3: Geopolitical De-Risking – The China Concentration Problem

US-China trade tensions, Taiwan contingency planning, export controls on advanced technology, and ESG-driven supply chain audits have made China concentration a board-level risk.

India is a democratic, English-speaking, rule-of-law market with strong US and EU relationships. It is not subject to Section 301 tariffs. It has no territorial disputes with the US or EU. For companies that need to demonstrate supply chain resilience to customers, regulators, and investors, India is the geopolitically safe alternative.

Reason 4: Domestic Market – Manufacturing Close to One of the World’s Largest Consumer Markets

India is a $3.7T economy growing at 6-7% per year. It will be the world’s third-largest economy by 2030. The Indian middle class (households earning $10K+ per year) is projected to reach 580 million by 2030.

For FMCG, automotive, electronics, and consumer goods manufacturers, India is not just a production platform – it is also a destination market. Manufacturing in India enables proximity to one of the few large consumer markets still in high-growth mode.

Reason 5: Existing Engineering Talent Base

India produces 1.5 million engineering graduates per year. The IT services industry – the world’s largest engineering outsourcing sector – has created a culture of process rigour, quality management, and technical problem-solving at scale.

Rolls-Royce, Boeing, and Airbus have engineering centres in India because the talent is there – and that same talent base supports manufacturing operational excellence.

Reason 6: Infrastructure – From Lagging to Competitive

India’s infrastructure gap was a legitimate barrier to manufacturing investment for decades. The gap is closing:

- National highways: 150,000+ km network, growing at 12,000 km/year under Bharatmala Pariyojana

- Dedicated Freight Corridors: Eastern DFC (Ludhiana-Kolkata) and Western DFC (Delhi-Mumbai) operational

- Ports: JNPT capacity expansion, new deep-draft berths at Mundra and Hazira, Sagarmala port connectivity programme

- Power: Installed capacity now 950 GW+; renewable energy (500 GW by 2030) reducing industrial power costs

Reason 7: The Ecosystem Effect – As Companies Come, the Ecosystem Deepens

Manufacturing clusters exhibit network effects. When Apple’s supply chain moves to India, Foxconn brings toolmakers, component suppliers, logistics specialists, and quality managers. Those capabilities then become available to the next company.

India crossed the critical mass threshold in electronics (Apple, Samsung, Foxconn, Jabil, Flex) around 2022-2023. The ecosystem effect is now operating.

Who Is Already There

- Apple: iPhone 15 and 16 series produced in India (Foxconn, Tata Electronics). India now accounts for ~14% of global iPhone production.

- Micron: $2.75B semiconductor assembly and test facility in Gujarat (operational 2025).

- Airbus: H125 helicopter final assembly in Bengaluru (partnership with Tata Advanced Systems).

- Rolls-Royce: Engineering and manufacturing operations in India; targeting India as a global supply chain hub for aero engines.

- Samsung: Largest mobile phone factory in the world by volume, Noida, India.

- Suzuki: 58% of global Suzuki production in India; investing Rs 35,000 Cr in new India capacity.

- Tata Electronics: Building India’s first domestic semiconductor fab (Dholera, Gujarat) and OSAT facility.

Key Takeaways

- Seven structural forces – demographics, policy, geopolitics, domestic market, talent, infrastructure, and ecosystem effects – are simultaneously driving India’s manufacturing rise.

- These are not cyclical factors; they are 10-20 year structural tailwinds.

- Category leaders across electronics, automotive, aerospace, and pharma have already made large-scale commitments.

- The ecosystem effect means the cost and risk of India entry is lower now than it was in 2020, and will be lower still in 2027.

- For global OEMs that have not started evaluating India manufacturing, the question is not whether – it is how fast.

FAQs

Q: Is India replacing China in manufacturing?

A: No – at least not in a 1:1 substitution sense. China’s manufacturing ($4T+ per year) is an order of magnitude larger than India’s ($500B). India is capturing the incremental shift in new investments and the re-sourcing of tariff-exposed, labour-intensive categories. China and India will coexist as complementary global manufacturing hubs.

Q: Which Indian state is best for manufacturing investment?

A: Tamil Nadu (electronics, automotive), Maharashtra (auto, industrial), Karnataka (aerospace, electronics), Telangana (pharma, aerospace), and Gujarat (chemicals, pharma, semiconductors) lead on policy stability, infrastructure, and supplier ecosystem depth.

Q: How long does it take to operationalise India manufacturing?

A: Via contract manufacturing: 3-6 months to first production. Via greenfield investment: 24-36 months. Via JV with existing Indian partner: 12-18 months.